In mid-2020, Securities and Exchange Commission (SEC) Rule 606(b)(3) came into full implementation. Rule 606(b)(3) (aka “Institutional 606”) adds an impressive data source for the buy side to help them navigate the increasingly complex world of order-routing analysis, execution quality review, conflict of interest management, and information leakage minimization. However, the information contained in the Institutional 606 reports is only delivered upon request by the buy side, so the question has to be asked – will the buy side be looking to the sell side to provide these reports?

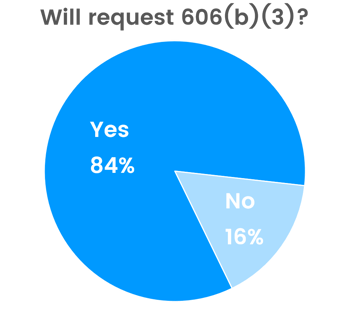

A recent Greenwich Associates report answers this question with a resounding “yes”! According to our research, 84% of our buy side respondents plan to request the Institutional 606 reports from their brokers. Even more telling, over the next year, an astonishing 73% of respondents intend to seek information above and beyond that required by the rule itself. Such information includes so-called “look-through” data which traces the entirety of a parent order through all of its routes and execution destinations.

And the buy side isn’t just going to be pulling these reports to meet a check-the-box exercise. Nearly 40% of respondents believe this information will be important or very important when determining their best execution protocols.

Buy side firms may, either directly or via their vendor partners, use the Institutional 606 data to confirm that their orders are being handled pursuant to their instructions, review if there is overweighting to destinations due to rebates or other economic incentives, and even develop their own broad-based analytics over a course of time. Moreover, these data points can also allow for a more direct head-to-head comparison of brokers by the buy side.

The road to approval of the Institutional 606 rule was long and protracted. However, at the end of this process, the buy side has been given a tool that provides firms of all sizes a standardized report on how their orders are handled by their brokers. Although the reports do not necessarily provide everything an institution needs to know in isolation (they do not capture intent of the parent order, for example), they create a golden opportunity for firms to ensure they are having an informed discussion with their brokers on a regular and routine basis. Ultimately, this type of communication should benefit both sides, leading to better execution across the board – which, after all, is the goal.