In our recent comment letter to the SEC, we are in support of NASDAQ’s proposed new order type the Midpoint Extended Life Order, AKA MELO.

MELO is designed to have market participants commit orders to a minimum half-second holding period with executions at the midpoint of the NBBO. We support MELO because we believe it can be a valuable tool for investors seeking liquidity in size. Having the midpoint of the NBBO pricing and the required holding period, MELO has the potential to attract long term investors to the NASDAQ. Especially in a time when institutional order flow is challenged by market participants trading in small size, “off exchange”, and with a much shorter investment time horizon.

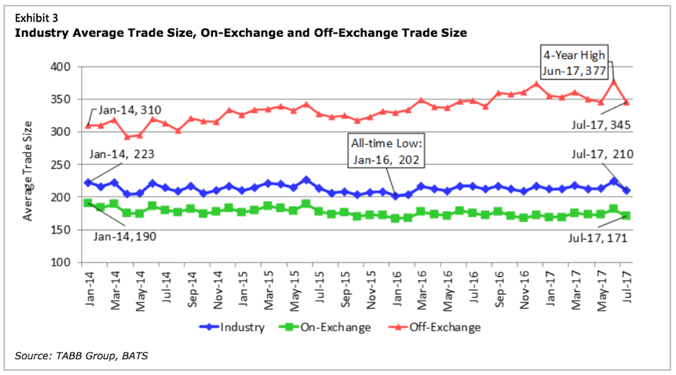

According to Tabb’s Q2 2017 Equity Digest, in June 2017 average on-exchange trade size was 182 shares while off-exchange trade size reached its highest trade size in 4 years, 377 shares.

We believe MELO will attract market participants interested in executing in block size. Often our broker-dealer clients are attempting to execute orders for large institutional investors and increasing their opportunity to source quality liquidity from other long-term investors is of critical importance. MELO’s holding period and executing at the midpoint of the NBBO provides long-term institutional investors interested in trading in size an opportunity to find the other side of the trade on-exchange, with minimal information leakage in a more equitable and transparent environment, counteracting the proliferation of off-exchange, private trading venue with non-transparent rulesets and potential disclosure and conflicts of interests.

Clearpool’s algorithms continuously adapt to market structure when sourcing liquidity. Therefore, we believe an important feature of MELO is the ability for market participants to cancel orders during the holding period. Our customized routing protocols will seek the most opportune times to capture liquidity, but while we make seek liquidity via a Midpoint Extended Life Order our algorithms will continue to work across venues sourcing liquidity to obtain best execution for our clients. In the event better quality liquidity can be captured at an alternate venue we want the option to cancel our order from NASDAQ and reallocate the shares.

To learn how Clearpool’s Algorithms adapt to market structure request a demo.

To read the full comment letter click here.